The Watchdog — Home and Abroad

Scott B. MacDonald, Ph.D. — February 2, 2026

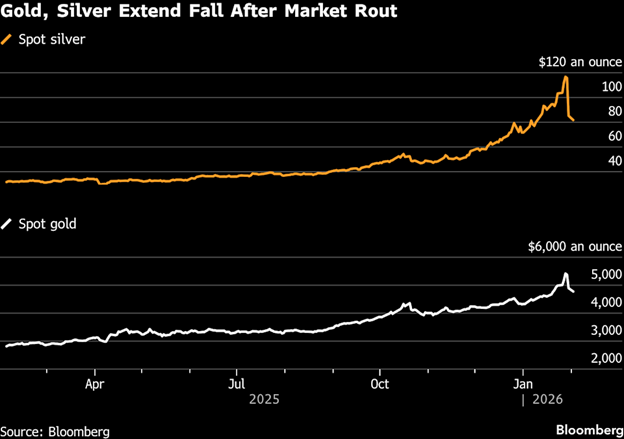

Summary: This week is likely to be dominated by earnings (Alphabet, Amazon and Palantir), a further look into how AI is playing out on company balance sheets, more economic data releases, and the US partial government shutdown (which we expect to be short-lived). The big data drops are going to be on Friday’s jobs report (consensus is looking at 65,000 jobs added), consumer sentiment from the University of Michigan, and reports on manufacturing and services. Eyes are also going to be on gold and silver, which recently had a historic upward run and then a major plunge. On the geopolitical front, Greenland and Venezuela remain points of concern, though they have become more backburner issues compared to Iran.

The new man at the Fed. The big news late last week was that President Trump nominated Kevin Warsh to head the Federal Reserve. Who is he? Warsh was on the Fed Board of Governors from 2006 to 2011, where he was a monetary “hawk”; was active in the 2008 financial crisis in designing and implementing emergency lending programs; and prior to government service worked at Morgan Stanley. He holds a degree in Public Policy from Stanford University and a law degree from Harvard University. Like Treasury Secretary Scott Bessent, Warsh is also a protégé of the billionaire investor Stanley Druckenmiller.

Warsh has been a critic of the Fed, warning that large-scale asset purchases and near-zero benchmark interest rates ran the risk of distorting markets and eroding long-term price stability. The Fed’s balance sheet now stands at roughly $6.6 trillion. It peaked at close to $9 trillion in 2022 and was under a trillion before the 2008 financial crisis.

Chairman Powell’s term ends in May, when it is assumed that Warsh will be made the leader. There may be a wrinkle in that the Trump administration’s criminal investigation into Powell raised alarm with politicians, economists and business leaders. More importantly, North Carolina Republican Thom Tillis and other Republican leaders said they will oppose all nominees to the Fed chair until the investigation is concluded. Tillis did indicate that Warsh is a “qualified nominee with a deep understanding of monetary policy,”

What does Smith’s think? Although concerns exist that Warsh’s selection will end the central bank’s independence, that view is simplistic. Yes, he has recently voted to cut rates in the Fed’s FOMC meetings and is critical of the central bank’s mission creep, but his track record indicates that he has been open to changing his stance. Equally important, his appointment itself does not constitute an end of Fed independence. He will be presiding over a committee of 12 voting members and must consider the views of non-voting FOMC members. The big question is how much Warsh can push the Fed toward lower rates, a challenge complicated by the potential that an AI-induced productivity boom could stoke inflation. His appointment may not be as much of a slam dunk for the Trump administration as critics see it, but it could see an overhauling of the institution’s mission. We expect 1 to 2 cuts in rates in 2026.

Gold – Ouch! Last week gold and silver were on a tear, hitting record prices. That extraordinary run ended abruptly on Friday. Silver fell 26%, its largest fall ever. Gold fell 10% on its worst day in a decade. Some of the losses were clawed back on Monday. The main drivers for the upward price movement were geopolitical upheaval, US dollar debasement and concerns over the Fed’s independence. That situation changed when President Trump announced Warsh to become the next Fed chairman. Two factors are worth considering: gold and silver had become crowded trades with everyone piling into them. In this, something like Warsh’s appointment which reduced uncertainty, broke the streak. The other factor, which is more in the realm of rumor, was that much of the trade was pumped up by hot money from speculators in China.

What does Smith’s think? Geopolitical uncertainty will remain a factor and US economic policy remains relatively unpredictable, which are likely to keep gold and precious metals attractive hedges, but not at their current levels.

Abroad – Headlines

Iran – The Ongoing Headache. The theocratic regime in Iran is wounded. The government, headed by Supreme Leader Ali Khamenei, is hugely unpopular, as most Iranians see it as corrupt and its leadership divorced from the harsh economic realities facing the population. The dissatisfaction led to a popular revolt in early 2026, which was ruthlessly crushed, leaving by some accounts between 30,000-50,000 killed. President Masoud Pezeshkian, who serves at the pleasure of the Supreme Leader, acknowledged the need for change and called for the formation of political parties and an end of the screening of electoral candidates. While Pezeshkian can be ignored, the US cannot, especially as a US aircraft carrier group has arrived in the region.

What does Smith’s think? President Trump has indicated that his administration is in talks with the theocratic regime to strike a deal that further denigrates Iran’s nuclear program. The theocratic regime must consider hard facts: pressure on the economy may ignite new unrest as everyday staples are scarce and US military strikes would only aggravate this situation. For its part, Iran’s Supreme Leader Khamenei has warned that any attack on his country would spark a regional conflict. While Iran continues to have military assets throughout the rest of the region that can inflict damage, the punch they offer is much less than it was last year. Khamenei and his ilk face tough decisions between defiance and another round of socio-economic upheaval, while contending with a US president has little regard for the niceties of international law in getting what he wants (as with Venezuela). Moreover, while regional governments do not want to see another war in the Middle East, it is doubtful that any of them would shed any tears for an Iranian regime which has interfered in their affairs for decades. Iran’s leadership may be more inclined to take Winston Churchill’s advice, “Jaw-jaw is better than war-war”.

China calls for the renminbi to attain global reserve currency status. China’s Xi Jinping is calling for the renminbi to be adopted as a global reserve currency. This fits into China’s push to carve out a greater role in the international monetary system. As China’s president stated, the country needs to have a “powerful currency” that could be “widely used in international trade, investment and foreign exchange markets, and attain reserve currency status.” Since the Russian invasion of Ukraine in 2022, the renminbi has become more widely used as a trade finance currency, including outside of Asia.

What does Smith’s think? China understands major shifts are occurring in the global economy. These include a new and unpredictable tariff regime in the US, a willingness by other economies to derisk from the US, and the development of new trading relationships (as reflected by the EU-India and Canada-China trade deals). Yet the renminbi is the world’s sixth global reserve currency, at only 1.93%. It has a long way to go before eclipsing the dollar, which accounts for 57% of global reserves, down from 71% in 2000. The euro stands at around 20%. We concur with Han Shen Lin, China country director at The Asia Group: “Xi’s rhetoric won’t flip global foreign exchange markets today, but it cements a long-term tilt investors are already sniffing out. Overall, Beijing senses the dollar’s shine isn’t unblemished and will nudge its currency forward.” Something to watch.

Venezuela – new oil legislation. Acting President Delcy Rodríguez signed a law that opens Venezuela’s oil sector for private companies (including foreign ones) to owning the production and sale of oil, ending the state-owned PDVSA’s monopoly over those activities.

What does Smith’s think? This is a positive development, but political risk remains high because $billions are needed to upgrade infrastructure and considerable legal work remains to remedy President Hugo Chávez’s earlier nationalization of assets owned by Western firms, including ExxonMobil and ConocoPhillips. Venezuela has a long way to go to catch up with more stable and welcoming energy investment environments in Guyana, Brazil, Argentina and Suriname.